Table of Contents

In The Psychology of Money book summary, we distill the key insights from Morgan Housel’s “The Psychology of Money“. In a world obsessed with financial formulas and complex investment strategies, Housel offers a refreshing and insightful alternative way of thinking about money.

The book shifts the focus from technical expertise to the often-overlooked realm of human behavior, exploring how our emotions, biases, and personal histories shape our financial decisions.

“Doing well with money has a little to do with how smart you are and a lot to do with how you behave”

Beyond Intelligence and Education

The book opens with a striking contrast – the stories of Ronald Read, a seemingly ordinary janitor, and Richard Fuscone, a highly educated and successful Wall Street executive. Read, through decades of patient saving and investing in blue-chip stocks, quietly amassed an $8 million fortune, while Fuscone, despite his privileged background and sharp intellect, ended up bankrupt.

These contrasting narratives highlight a core premise of the book – doing well with money is less about intelligence and more about behavior. A genius who can’t control their emotions can be a financial disaster, while ordinary people with no formal financial education can achieve extraordinary wealth through disciplined habits and a sound understanding of human psychology.

“The hardest financial skill is getting the goalpost to stop moving.”

The Intricate Dance of Luck and Risk

Housel challenges readers to acknowledge the often-unpredictable roles of luck and risk in financial outcomes. Bill Gates’ immense success, for example, was undeniably influenced by his one-in-a-million chance of attending one of the few high schools with a computer in 1968.

Conversely, Gates’ brilliant friend, Kent Evans, tragically died in a mountaineering accident, highlighting the indiscriminate nature of risk.

These stories underscore the danger of assuming that success is solely a product of hard work and intelligence. When we fail to account for the role of chance, we risk misjudging both our own potential and the achievements of others.

Housel suggests focusing less on individual case studies and more on broad patterns of success and failure to glean more actionable insights.

The Enigmatic Power of Compounding

The book emphasizes the incredible, yet often counterintuitive, power of compounding. Much like the slow, steady force of ice ages that shape the earth’s surface, compounding allows small, consistent gains to accumulate into extraordinary results over time. Warren Buffett’s immense wealth, for instance, stems not just from his investing acumen, but from the fact that he’s been investing consistently since childhood.

Housel uses a thought experiment to illustrate the profound impact of an early start. Had Buffett begun investing at age 30 with a modest net worth, even with his exceptional investment returns, his wealth would have been significantly lower.

“There is no reason to risk what you have and need for what you don’t have and don’t need.”

Similarly, Jim Simons, despite generating higher annual returns than Buffett, has a smaller net worth because he began investing later in life.

The counterintuitive nature of compounding often leads us to underestimate its potential, causing us to prioritize short-term gains over long-term consistency. The most effective investment strategy, Housel suggests, might simply be to “Shut Up And Wait,” allowing compounding to work its magic over time.

The Art of Staying Wealthy

While many books focus on how to get rich, “The Psychology of Money” addresses the equally important challenge of staying wealthy. Housel argues that a combination of frugality and paranoia is essential for preserving wealth.

He draws a parallel between personal finance and the way the U.S. economy has grown over the past 170 years. Despite enduring numerous setbacks, from wars and recessions to pandemics and social unrest, the economy has consistently trended upwards. Similarly, individuals who achieve lasting financial success often do so by embracing a long-term perspective, accepting setbacks as part of the journey, and focusing on minimizing losses.

Housel likens this approach to the strategy of successful card counters in Las Vegas. While they understand the odds are in their favor, they never bet everything on a single hand. They recognize the importance of “room for error” – leaving themselves a buffer to withstand inevitable losses and continue playing the game. This same principle applies to investing, where a margin of safety helps protect against unforeseen events and allows for compounding to continue uninterrupted.

The Allure of Pessimism

Despite the undeniable progress humanity has made in areas like economics, technology, and healthcare, pessimism often receives more attention than optimism. Housel suggests several reasons for this.

First, pessimistic narratives tend to be more dramatic and attention-grabbing. Second, they often tap into our inherent negativity bias – our tendency to focus more on negative events than positive ones. And third, progress often happens slowly and gradually, while setbacks tend to be sudden and dramatic.

This allure of pessimism can be financially dangerous, leading us to underestimate the long-term potential for growth and make decisions based on fear rather than rational analysis

“Wealth is what you don’t see.”

Aligning Money with Your Values

Ultimately, “The Psychology of Money” encourages readers to define financial success in a way that aligns with their personal values. Housel emphasizes that money is merely a tool, and its true value lies in its ability to provide freedom, security, and the opportunity to pursue a fulfilling life.

He advises readers to prioritize experiences over possessions, recognizing that material wealth often fails to deliver the respect and admiration we crave. Instead, he suggests focusing on cultivating qualities like kindness, humility, and empathy, which ultimately bring greater fulfillment than fleeting displays of affluence.

Key Insights

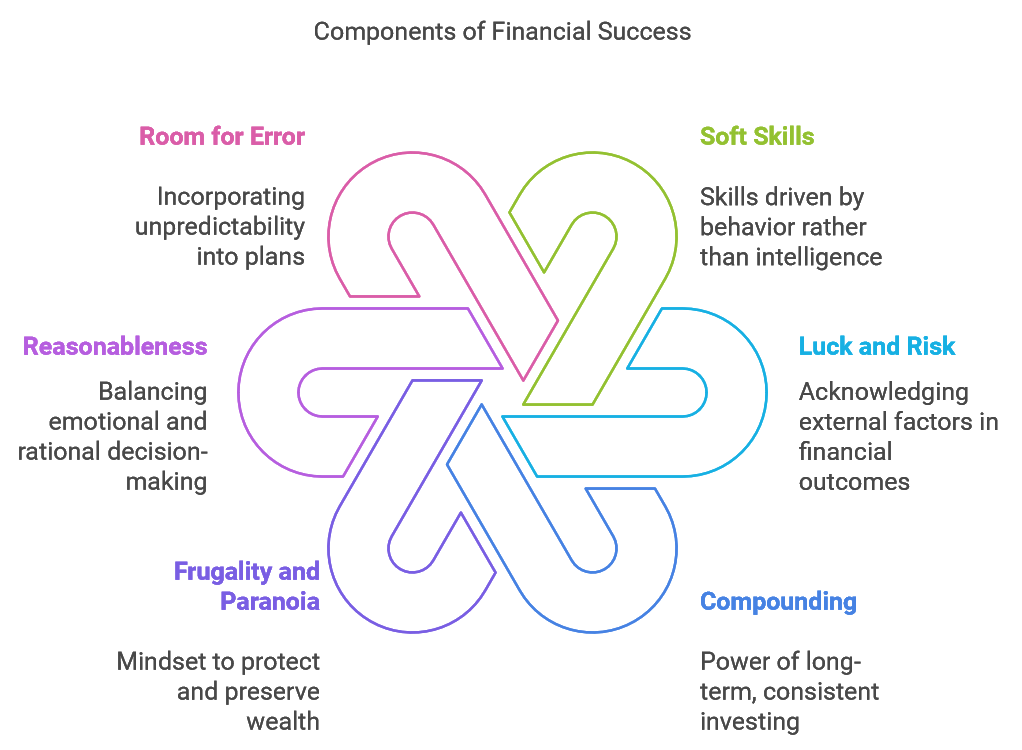

“The Psychology of Money” offers a wealth of insights into the human side of finance, challenging readers to:

- Recognize that financial success is a soft skill, driven by behavior rather than intelligence or education.

- Acknowledge the roles of luck and risk in financial outcomes, avoiding the trap of attributing all success to individual effort.

- Embrace the power of compounding through long-term, consistent investing.

- Develop a mindset of frugality and paranoia to protect and preserve wealth.

- Prioritize reasonableness over rationality, recognizing the emotional component of financial decision-making.

- Incorporate room for error into financial plans, acknowledging the unpredictable nature of life.

- Define “enough” financially and align financial decisions with personal values.

- Resist the allure of pessimism and maintain a long-term perspective grounded in optimism.

- By understanding the psychological factors that drive our financial decisions, we can make more informed choices, avoid common pitfalls, and cultivate a healthier and more fulfilling relationship with money.

“The ability to do what you want, when you want, with who you want, for as long as you want, is priceless. It is the highest dividend money pays.”

Who should read The Psychology of Money?

- People who are new to personal finance: The book uses short stories to discuss important, yet often counterintuitive, aspects of personal finance, especially for novices. For instance, it helps readers understand the importance of saving and investing for retirement, even if retirement may seem far off.

- Experienced investors: While the book is helpful for beginners, it also provides valuable insights for those already familiar with investing. The book points out that even seasoned investors can learn from the book’s exploration of behavioral skills and the psychological factors influencing financial decisions, like risk tolerance, regret minimization, and the need for a margin of safety.

- Anyone interested in understanding the role of luck and risk in financial success: The examines the often-overlooked influence of luck and risk in financial outcomes. It provides examples, like Bill Gates’s early access to computers and Ronald Read’s patient, long-term investing approach, to demonstrate how external factors can contribute to both success and failure.

- People who struggle with managing their emotions related to money: The book highlights the significance of understanding and managing emotions like greed, fear, and optimism when it comes to money. By recognizing these emotional influences, readers can make more rational and informed financial decisions.

- Anyone seeking to improve their financial decision-making: The author asserts that the book’s main goal is to help readers make sounder financial choices by understanding the psychological aspects of money. It covers a range of topics, including saving, investing, and spending habits, providing actionable lessons to improve overall financial well-being.

- Individuals interested in the history and evolution of consumer behavior: The book delves into the historical context of American consumer behavior, exploring the factors that have shaped people’s attitudes towards spending, saving, and debt. Understanding this history provides valuable insights into current financial trends and decision-making patterns.

Overall, The Psychology of Money aims to provide a comprehensive understanding of the human factors that influence financial behavior.

It offers valuable insights for a wide range of readers, from those just starting to manage their finances to seasoned investors seeking to refine their decision-making processes.

Chapter Summaries and Key Takeaways From “The Psychology of Money”

Chapter 1: No One’s Crazy

This chapter introduces the idea that everyone approaches finances based on their own personal experiences, which represent a tiny fraction of what’s happened in the world but significantly shapes their financial outlook. People from different generations, upbringings, and economic environments learn different lessons about money.

These differences in experiences and learned lessons can lead to seemingly “crazy” financial decisions, but from the individual’s perspective, their actions are often rational based on their own limited understanding of the world. For instance, someone who lived through the Great Depression might be deeply risk-averse, while someone who grew up during a booming economy might be more comfortable with taking risks.

Key Takeaway: It’s crucial to recognize that people’s financial decisions are influenced by their unique life experiences, making it important to avoid judging others’ choices and focus on understanding their perspective.

Chapter 2: Luck & Risk

The story of Bill Gates, who attended a rare school with a computer, illustrates the significant role luck plays in success. On the flip side, his friend Kent Evans, equally brilliant, died young in a mountain climbing accident, highlighting the constant presence of risk in life.

This chapter emphasizes that attributing outcomes solely to talent or hard work ignores the powerful influence of luck and risk. For example, investors who make seemingly brilliant decisions might just be lucky, while others who make good choices might face unforeseen risks leading to failure.

Key takeaway: When evaluating both your own and others’ financial successes or failures, recognize the role of luck and risk. Focus on broad patterns of success and failure, rather than specific individuals or case studies, as these patterns are more likely to yield actionable insights.

Chapter 3: Never Enough

Two contrasting stories highlight the dangers of not having “enough.” Rajat Gupta, a successful businessman, risked and lost everything due to insider trading, while Bernie Madoff’s Ponzi scheme led him down a similar path of ruin. This chapter emphasizes that the pursuit of more, even for those who already have plenty, can lead to disastrous consequences. There’s a real psychological challenge in getting the goalpost to stop moving.

Key Takeaway: Define what “enough” means for you and recognize the dangers of chasing endless wealth. Understand that some things—reputation, freedom, relationships, happiness—are invaluable and should not be jeopardized for financial gain.

Chapter 4: Confounding Compounding

Compounding, the process of earning returns on your returns, is compared to ice ages that gradually shaped the Earth. Just as small changes over time can create dramatic geological transformations, consistent investing over long periods leads to astounding wealth accumulation. This chapter uses Warren Buffett as an example, emphasizing that his success is rooted not just in skill but also in decades of compounding.

Key takeaway: Patience and time are crucial for compounding to work its magic. Avoid getting caught up in chasing high returns that are difficult to sustain and focus on earning consistent returns over long periods.

Chapter 5: Getting Wealthy vs. Staying Wealthy

This chapter contrasts the stories of Jesse Livermore, a brilliant stock trader who made and lost a fortune multiple times, with Ronald Read, a janitor who amassed millions through consistent saving and investing. It highlights the difference between getting wealthy, which can involve luck and risk, and staying wealthy, which requires a combination of frugality and paranoia. The author explains that “survival” is key to financial success, as it allows you to stay invested for the long term and reap the rewards of compounding.

Key Takeaway: Building wealth requires a different mindset than maintaining it. Focus on strategies that ensure long-term survival, emphasizing the importance of minimizing risks that could lead to catastrophic losses.

Chapter 6: Tails, You Win

The chapter introduces the “long tail” concept, explaining that extreme and infrequent events, often outliers, disproportionately drive outcomes. Examples range from venture capital, where a handful of investments drive most returns, to art collecting, where a few pieces in a large portfolio determine overall success. The author shows that even in established markets like the Russell 3000 Index, a small percentage of companies generate the majority of returns.

Key takeaway: Recognize that a few outlier events—”tails”—often determine overall success. This means accepting that most things will fail and focusing on positioning yourself to benefit from the few that succeed.

Chapter 7: Freedom

The true value of money lies in its ability to provide control over your time, granting you the freedom to pursue passions, spend time with loved ones, and reduce stress. The chapter tells the story of Derek Sivers, who saved aggressively to create financial independence, allowing him to pursue entrepreneurial ventures.

The author emphasizes that this “freedom dividend” is a far more valuable return than chasing material possessions. Additionally, the chapter explores the changing nature of work, where knowledge-based jobs make it difficult to detach, leading to a constant feeling of being “on the clock.”

Key Takeaway: Align your financial goals to maximize control over your time, enabling you to pursue what truly matters. The ability to do what you want, when you want, with whom you want, is the ultimate reward money can buy.

Chapter 8: Man in the Car Paradox

This chapter challenges the idea that expensive possessions, like luxury cars, automatically bring respect and admiration. It argues that people who buy flashy items often seek validation from those who can’t afford them, creating a paradoxical situation where the admiration comes from those you might not actually respect. The author suggests that genuine respect comes from qualities like kindness, humility, and empathy, not material wealth.

Key takeaway: Focus on building genuine relationships and respect through character, rather than seeking validation through material possessions. True admiration comes from those whose opinions you value, and it’s rarely earned through flashy displays of wealth.

Chapter 9: Wealth is What You Don’t See

The chapter emphasizes that true wealth is often invisible. Many seemingly modest individuals are wealthy due to their saving and investing habits, while some who flaunt their riches might be living on the brink of financial ruin. The author explains that wealth is built by not spending the money you have, and it’s often hidden in assets like investments and savings.

This invisibility makes it harder to learn from others’ financial success, as we often only see the outward signs of wealth, not the underlying habits that created it.

Key Takeaway: Focus on building true wealth through savings and smart financial decisions, recognizing that outward appearances can be deceptive. Avoid judging others’ financial success based solely on what you see, and concentrate on developing the habits that lead to long-term wealth.

Chapter 10: Save Money

This chapter highlights the crucial role of savings in building wealth. It argues that saving is more important than income or investment returns. The author explains that a high savings rate enables you to accumulate wealth even with modest earnings. The chapter uses the analogy of energy efficiency, arguing that reducing your needs is more impactful than acquiring more resources.

Furthermore, saving provides a safety net for unexpected events and offers flexibility to pursue opportunities that align with your values, even if they don’t come with a high salary.

Key Takeaway: Prioritize saving as a cornerstone of your financial strategy. It’s a hedge against life’s unpredictability and provides the flexibility to pursue a life that aligns with your values.

Chapter 11: Reasonable > Rational

This chapter argues that being “reasonable” is often more important than being strictly “rational” when making financial decisions. The author uses the story of Julius Wagner-Jauregg, who cured syphilis with malaria, to illustrate this point. While seemingly “crazy,” his approach yielded positive results.

The chapter goes on to explore the concept of leverage and how, while mathematically advantageous in certain situations, it can lead to devastating outcomes when things go wrong. People often overestimate their ability to handle risk, making seemingly rational decisions that can backfire.

Key Takeaway: Incorporate both logic and human behavior into your financial decisions. While rational calculations are important, consider your emotional capacity for risk and aim for strategies that are sustainable in the long run.

Chapter 12: Surprise!

This chapter emphasizes the inherent unpredictability of the future. Using examples like the September 11th attacks and the Fukushima nuclear disaster, the author highlights that even careful analysis and planning can fail to account for unforeseen events. The chapter argues that clinging to past trends and assuming the future will resemble the past can lead to significant errors in judgment. It also points out that successful investors are often those who are comfortable with uncertainty and willing to adapt to changing circumstances.

Key Takeaway: Embrace the unpredictable nature of the world and prepare for surprises. Be skeptical of forecasts that claim certainty, especially those based solely on past trends. Instead, focus on building resilience and adaptability into your financial plans.

Chapter 13: Room for Error

The chapter draws parallels between successful blackjack card counters and prudent investors, highlighting the importance of “room for error.” Just as card counters know they can’t predict every hand with certainty and bet accordingly, investors should acknowledge that their forecasts are not guarantees.

The author explains that unexpected events and unforeseen risks are inevitable, making it crucial to build a margin of safety into your financial decisions. This involves expecting things to go wrong, saving more than you think you need, and diversifying your investments to avoid single points of failure.

Key Takeaway: Plan for uncertainty and build a margin of safety into all your financial decisions. This helps protect you from unexpected events and allows you to stay invested even when things don’t go as planned.

Chapter 14: You’ll Change

This chapter underscores the fact that people evolve over time, and financial plans made in the past may no longer align with current priorities. The author explains that clinging to outdated goals due to “sunk costs” can prevent you from making necessary changes. A key takeaway is that financial plans are not static and should adapt to your evolving values and circumstances.

This involves regularly reassessing your goals, being willing to abandon those that no longer serve you, and avoiding feeling obligated to stick with past decisions simply because you’ve already invested time or money.

Key takeaway: Your financial goals should evolve alongside your personal growth. Don’t be afraid to let go of outdated plans, even if you’ve already invested significant time or resources.

Chapter 15: Nothing’s Free

This chapter highlights the principle that everything in finance comes with a price, even if it isn’t immediately apparent. It uses the downfall of General Electric, once a corporate giant, as an example of how pursuing short-term gains at the expense of long-term sustainability can lead to disastrous consequences. The author explains that seeking high returns without accepting the associated risks is akin to trying to get something for nothing, and it rarely ends well. Instead, successful investors understand that volatility and uncertainty are inherent costs of pursuing long-term growth.

Key takeaway: Be prepared to pay the price for success, acknowledging that volatility, uncertainty, and setbacks are often part of the journey. Avoid strategies that promise high returns without acknowledging the associated risks.

Chapter 16: You & Me

This chapter examines the dynamics of financial bubbles, explaining that they arise not just from greed, but also from differing investor goals and time horizons. Using the dot-com and housing bubbles as examples, the author illustrates how short-term speculation can drive prices far beyond their intrinsic value. The chapter argues that when investors with vastly different time horizons participate in the same market, it can create a disconnect between perceived value and long-term sustainability.

Key Takeaway: Understand your own time horizon and invest accordingly. Don’t let the actions of short-term speculators influence your long-term investment strategy, and avoid getting caught up in bubbles driven by unsustainable price increases.

Chapter 17: The Seduction of Pessimism

This chapter explores the allure of pessimism, arguing that it is often more persuasive than optimism, especially in the realm of finance. The author suggests that pessimistic narratives tend to be more dramatic and attention-grabbing, while optimistic viewpoints require considering long-term trends that are easily overlooked. The chapter uses examples like Japan’s post-war economic boom and the advancements in medicine to illustrate how progress is often gradual and less noticeable than sudden, negative events.

Key Takeaway: Maintain a balanced perspective when evaluating financial information. Be aware of the tendency for pessimism to overshadow optimism and recognize the power of long-term growth, even amidst short-term setbacks.

Chapter 18: When You’ll Believe Anything

This chapter delves into how people rationalize their financial decisions, particularly when faced with limited control and high stakes, making them more likely to believe in appealing but often false narratives. The author illustrates this with the story of Ali Hajaji, who resorted to a harmful folk remedy for his sick son due to his desperate circumstances. The chapter also draws parallels to historical events like the Great Plague of London, where people readily embraced quack cures in the face of a deadly disease. It argues that financial decisions are often made under similar conditions, with high stakes and limited information, making people vulnerable to believing in stories that promise easy solutions or unrealistic outcomes.

Key takeaway: Recognize your own vulnerability to believing appealing financial narratives, especially when you feel a lack of control or face high stakes. Seek out diverse perspectives, be critical of information that confirms your biases, and focus on building financial independence to reduce your susceptibility to these influences.

Chapter 19: All Together Now

This chapter emphasizes the limitations of individual perspectives and highlights the importance of recognizing that everyone has an incomplete view of the world. The author uses the analogy of explaining complex concepts to a young child, who lacks the necessary context and experience to understand.

The chapter also explores how history, despite being a recounting of past events, is often interpreted subjectively, with people seeking to confirm their existing beliefs. This underscores the challenge of making sense of complex systems like the financial markets, where numerous factors influence outcomes, and individual perspectives are inherently limited.

Key Takeaway: Acknowledge the limitations of your own perspective and be open to understanding different viewpoints. Recognize that financial decisions are often made within a complex system with numerous interacting factors, and your understanding of that system is inherently incomplete.

Chapter 20: Confessions

In this chapter, the author offers a personal perspective on his own financial philosophy and approach to money management. He emphasizes the importance of aligning financial decisions with personal values, highlighting his prioritization of financial independence over chasing high returns or maximizing wealth.

The chapter also advocates for simplicity in investing, favoring index funds over actively managed portfolios and complex trading strategies. The author stresses the importance of saving consistently and focusing on what you can control—savings rate, patience, and a long-term perspective—rather than trying to predict market movements or time the market.

Key Takeaway: Develop a personal financial philosophy that aligns with your values and goals. Prioritize financial independence, focus on what you can control, and embrace a long-term, patient approach to investing.

Postscript: A Brief History of Why the U.S. Consumer Thinks the Way They Do

This section traces the historical events that shaped the modern American consumer mindset. It begins with the post-World War II era, marked by pent-up demand and a surge in consumer credit fueled by government policies like the GI Bill. The author describes how this led to an economic boom, with increased production and consumption driving widespread prosperity.

However, subsequent decades witnessed a shift from an industrial economy to a knowledge-based one, with income and wealth becoming increasingly concentrated at the top. This contributed to rising debt levels as people tried to maintain their living standards, culminating in the 2008 financial crisis. The chapter concludes by suggesting that while the current economic paradigm is unsustainable, changing it will be difficult due to entrenched interests and policies.

Key Takeaway: The modern American consumer mindset is a product of specific historical events and policy decisions. Understanding this history provides context for current economic challenges and the need to address underlying issues like income inequality and unsustainable debt levels.

Enjoyed The Psychology of Money book summary? Check out these other book summaries on managing your money here

You may also like:

Leave a Reply